For you to quit your job, you will need another equivalent source of income to fill the gap where your monthly paycheck used to be. Traditionally, this set-up was known as retirement. You retire, and as a result of having paid into your government’s pension system for your working life, they give you an annual income to finance your lifestyle in your final, non-working years. The potential problem that many will experience is that the money they receive from their government pension is often less than half of what they received during their working years. Or they are not happy to wait until their 60s or even 70s to receive a government pension. The solution is to take charge of your own financial independence in Japan.

Reductions in benefits in Japan – Threat To Financial Independence

Many of the world’s countries are laden with a colossal amount of debt. In aim of keeping the economic plates spinning and avoiding crises, alongside intervention and policy changes from central banks, governments look to reduce spending wherever possible. One of the results of this is a reduction in pension benefit and pushing back the age of availability. You will likely pay the same or more into the system as your parents did, but have to wait longer, to receive less. In the wealthy countries it studied, the OECD found that the pension reforms of the 2000’s will cut retirement benefits by an average 20 percent.

Individual savings deficits

Financial literacy remains low and few people save enough. An inherent distrust of the banking industry and investment markets following the global financial crisis has meant that people who do have the resources to invest often chose instead to have their money sit idle in the bank in cash. Millennials invest substantially less than previous generations and are more likely to spend their disposable income than buy assets. In the U.S., households took on an additional $5.4 trillion in debt — an increase of 75 percent — from the start of 2003 until mid-2008, according to the Federal Reserve Bank of New York.

Deterioration in company benefits

Companies have systematically reduced their employee benefits in Japan over the years, making personal savings more and more important for one’s financial independence. Defined Benefit Schemes which paid a lifetime income based on your annual salary in your final years of employment are becoming a thing of the past. As the job market is not as flush with opportunity as it was two decades ago, companies are able to scale back their employee benefits (which are focused on providing long-term benefits), and not experience a decline in applications in the short-term; after all, as an unemployed worker, you are likely more concerned about paying your mortgage repayments this month, than you are about paying the bills in your retirement.

If you wish to at least continue your current lifestyle in later life, without having to scale back your spending or reduce your standard or living, then your only option is to make financial plans for yourself. You will have to save money, and you will have to invest money. The spending sacrifices you will be making now are the ensure that you do not have to make sacrifices in the future. Think of it as a pre-payment; a gift from present you to future you.

How Much Money Do I Need To Reach Financial Independence In Japan?

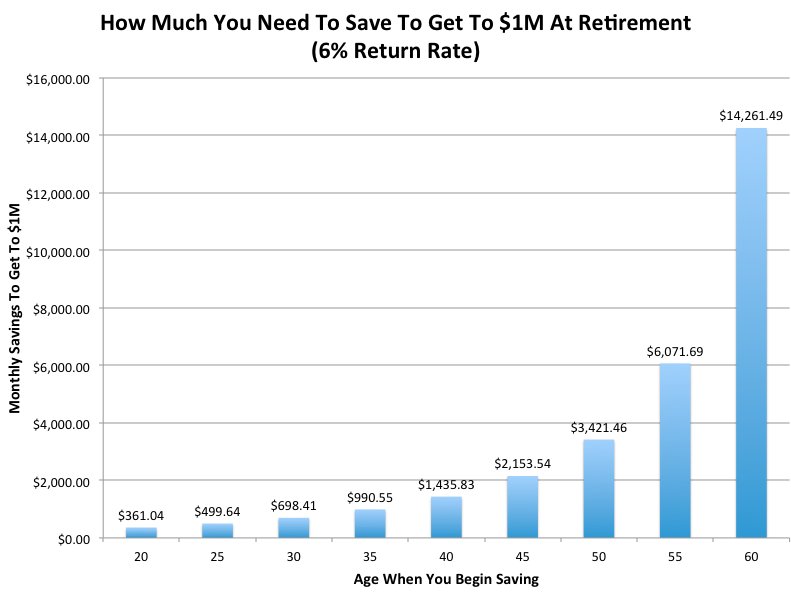

Depending on who you ask, you will be told a different calculation, or a different method to use to work out how much you will need to have in your bank account. Lets assume that they are all correct. Many people will be inclined to question or criticize a method which produces a large number and will often come up with excuses like “I can probably live on less than I’m spending now anyway“, “the kids will be grown up by then so it will actually cost less“, or “we could always move somewhere cheaper“. These are all natural self-preserving reactions to have when you are forced to stare down a large amount of money that you will actually need when you have no plan on how to actually accumulate it. Generally speaking as a rule of thumb, if the required sum at the end of your calculation is big, has 7 digits and seems unattainable, the likelihood is that your calculations have been correct. First, take a moment to see if you are on track at this point in time with your current savings and investments.

![]()

If you are not quite where you need to be, then you should reconsider your current financial behaviors in aim of creating, or freeing up extra money each month that can go into a savings account of some kind. There is an old adage that if you are able to save 20% of your income for 30 years then you will be financially independent. Of course, if you are able to save more than this you could revise down the length of the journey. In reality however, short-term spending, various financial liabilities and fluctuations in disposable income will mean that the process is far less linear. People will also have differing standards of living that they want to have after the conclusion of their careers.

Talking to your financial advisor will help you to get a personalized answer so that you do not have to rely on template-responses online which often miss out important components such as tax and risk tolerance. As a springboard for conversation, many people will ask us how to get to one million dollars. Your biggest asset will be time: the longer you have until retirement in Japan, the less you need to invest each year to reach your goal of financial independence. The converse is however also true; the less time you have remaining, the more you will need to invest now.

Published: 12 March 2017